Pre-Judgment Interest

The time in between the due date of an invoice and the date that a client/customer actually pays can be a very long. It is also often a a very long time before a creditor will file a lawsuit on an unpaid invoice (if at all). It's even longer to actually get a judgment. There is a time-value to money, and the time before the amount due is actually placed in your hands is revenue lost.

Much less though if you get to charge interest on the unpaid account.

There are two methods of reducing this loss, by contract between the parties or by statute.

By statute is the most common method for calculating interest accrued between the time the customer first receives (and fails to pay) an invoice and the time there is actually a court judgment enforcing your right to be paid. The reason it is normally provided for by statute is that many invoices are by a simple service order or estimate. What is effectively a receipt rarely provides for interest on past due amounts and is often not even counter-signed by the customer/client. There just isn't a contractual agreement providing for interest. As such, the concept defaults to what statute provides.

The statute does provide some protection against the time loss value of the revenue, but it is not the most generous. Basically, per Texas Finance Code § 304.101 et seq, pre-judgment interest

1) Accrues at the prime rate established by Federal Reserve (currently 5.50%), but at a minimum rate of five percent (5%);

2) Only starts to accrue six months after the invoice is sent and remains unpaid;

3) Accrue until the date of judgment (at which point post-judgment rules apply);

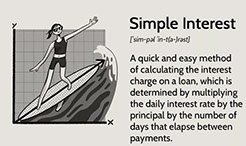

4) Is calculated as simple interest and is not compounded Texas Finance Code § 304.104(post-judgment interest is compounded annually Texas Finance Code §304.006); and

5) If the Defendant makes a settlement offer, interest does not accrue on the portion equal to the amount of the settlement offer while the settlement offer remains open. Texas Finance Code §304.105. (As such, it is always good for a Defendant to make a reasonable settlement offer if possible as it locks up some pre-judgment interest and also potentially avoids attorney's fees - depending on the amount of the final judgment.)

Also, one may note that the statute says it only applies to cases of wrongful death, personal injury or property damage. An unpaid invoice is not quite 'property damage'. However, In Texas, prejudgment interest is designed to compensate the plaintiff “for the defendant having beneficial use of the damage funds between the time of the occurrence and judgment.” Matthews v. DeSoto, 721 S.W.2d 286, 287 (Tex. 1986). “Prejudgment interest is not intended to punish the defendant's misbehavior”, but rather to “compensate[] the plaintiff for being denied the opportunity to invest and earn interest on the amount of damages.” Id. The Supreme Court of Texas recognizes two bases for the award of prejudgment interest: (1) prescription by statute; and (2) general principles of equity. Matter of Okedokun, 968 F.3d 378, 392 (5th Cir. 2020). Statutory prejudgment interest applies only in wrongful death, personal injury, property damage, and condemnation cases. Id. In contrast, equitable prejudgment interest “is available as a matter of course, absent exceptional circumstances.” Id.. “The Texas Supreme Court has made clear that the award of prejudgment interest, although equitable in nature, is not generally a matter for the trial court's discretion.” Executone Info. Sys., Inc. v. Davis, 26 F.3d 1314, 1330 --- As such, pre-judgment interest is available on an unpaid invoice.

Contractual Pre-judgment Interest

Whenever possible, it is always a good idea to write up your contracts and service orders with some terms that provide a penalty for late or failed payment (and have the customer counter-sign the service order as 'approval').

Whether characterized as a late charge or interest thereon, after the invoice is thirty days past due (which is better than the statutory 180 days), the parties may agree to an interest rate thereon that, for practical purposes may be up to 18%.

Some may try to tell you that rate is usurious. This is an answer that comes from knowing a only little bit of law.

The usury rate in Texas is ten (10) percent a year except as otherwise provided by law. Tex. Fin. Code Ann. § 302.001. The ten percent default usury rate means virtually nothing given that rate ceilings of Subchapter A of Chapter 303 of the Texas Finance Code create an exception to the usury rate rule that, more or less, swallows the rule whole. “Except as provided by Subchapter B [mostly related to credit cards], a person may contract for, charge, or receive a rate or amount that does not exceed the applicable interest rate ceiling provided by this chapter.” Tex. Fin. Code Ann. § 303.001. “The parties to a written agreement may agree to an interest rate . . . that does not exceed the applicable weekly ceiling.” Tex. Fin. Code Ann. § 303.002. So, basically, most loans can charge the weekly ceiling, which is generally going to be substantially higher than the ten (10) percent default usury rate, rendering the default rate rarely applicable.

The weekly rate can be found in the Texas Credit Letter, which can be found online: https://occc.texas.gov/publications/interest-rates. If one reviews the archived letters, they will see that the maximum allowable rate has been 18% forever ( -- 5% for judgments, although that has been creeping upward as of late).

Since the law does not provide for compounding of pre-judgment interest - don't do it in your contract or invoices.

281-408-3683

© 2015, 2022